2025 Crypto Predictions Review

An honest post-mortem of my 2025 crypto predictions, scoring what worked, what didn’t, and why.

Executive Summary

A deliberately contrarian macro call played out almost perfectly, rate cuts arrived without recession, equities benefited far more than crypto, and markets normalized rather than extended excesses.

After a brief Q1 drawdown, equities rebounded strongly, with the S&P 500 finishing up ~17%, squarely within the expected range and validating the broader moderation thesis.

Bitcoin remained the market anchor, but price outcomes were mixed; it briefly hit the bearish case near $126k, missed base and bull targets, and unexpectedly finished the year down ~4%.

ETF demand was structurally positive but materially weaker than expected and highly concentrated, resulting in a mixed score despite correct calls on market structure.

ETH outperformed expectations mid-year, driven not by ETFs but by large-scale accumulation from Ethereum-focused DATs, validating the directional price call and producing a rare window of ETH/BTC strength.

The memecoin supercycle thesis failed quickly as expected, while the AI-agent supercycle proved overly optimistic, collapsing early and wiping out over 80% of sector value.

The anticipated alt-L1 rotation never meaningfully materialized, but stablecoin growth surpassed expectations, DeFi TVL peaked as projected, and NFTs entered a sustained decline.

The most important trap was overestimating 2025 itself, a slower, underwhelming year with a late-Q4 peak — reinforcing the warning that expectation management mattered more than individual narratives.

As is tradition with my yearly investment memos, I revisit the predictions I made—not to brag or gloss over the misses, but to learn. The real value lies in looking back objectively at what worked, what didn’t, and, more importantly, why.

That process matters because improvement requires feedback. One of the most insightful explanations of this comes from a Veritasium video on what it actually takes to become an expert. Beyond the well-known “10,000 hours” popularized by Malcolm Gladwell, he highlights feedback as a critical ingredient. In other words, time alone isn’t enough—you need a feedback loop. This review is mine.

To keep things simple and honest, I’ll score each prediction on a scale from 1 to 5:

5 — Bullseye

3 — Directionally correct

1 — Completely off

Simple, structured, and transparent—so I can compound lessons, not just experience, and do better next time.

01 / Macro

Early in the year, I made a set of macro calls that were intentionally bold—and largely counter-trend at the time. My base case was that 2025 would be a much quieter year than most expected and, therefore, would feel disappointing to many given just how optimistic positioning was at the start of the year.

That context matters. These views were formed at the peak of the AI agent craze in crypto and the broader AI mania in equities. They also came in the immediate aftermath of Trump’s election win, just weeks before his inauguration. At the same time, the S&P 500 was sitting at all-time highs. With sentiment stretched and narratives firing on all cylinders, it was convenient—and widely assumed—that the party would simply continue.

Against that backdrop, I argued that rate cuts would primarily act as a tailwind for equities rather than crypto. The reasoning was simple: crypto increasingly trades on narratives, not fundamentals. That distinction mattered, and it became even more obvious as the year played out.

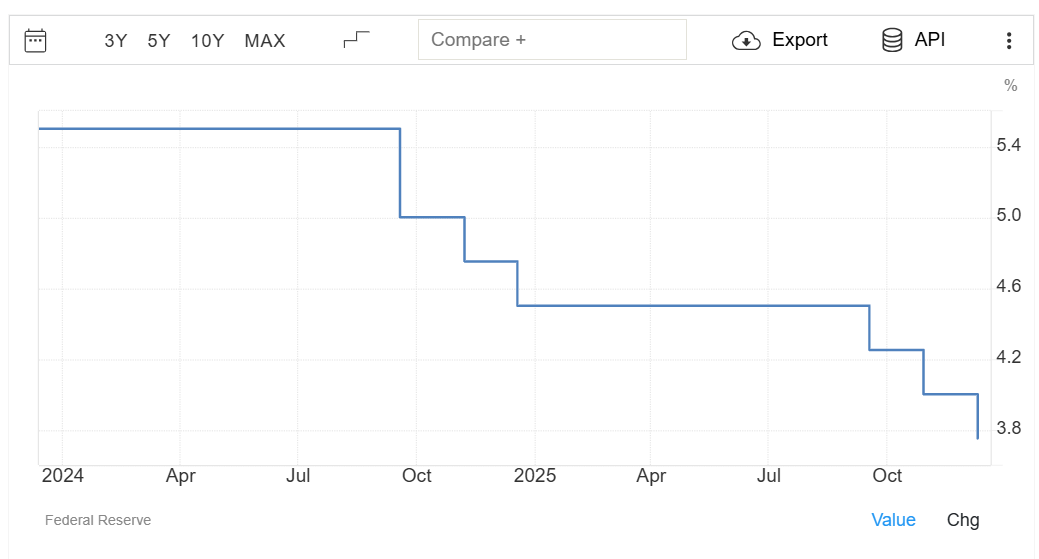

On rates specifically, my view was that we would see cuts in 2025. At the time, I wrote:

“I believe the Fed will cut rates more than twice this year, despite their recent messaging suggesting otherwise.”

The prevailing posture then was the opposite. Consensus held that rates wouldn’t be cut at all, or that any cuts would only come in response to a recession or stagflation. However, neither scenario materialized.

Instead, the Fed held rates steady through the early part of the year before delivering three consecutive cuts in the second half. Each was a 25 bps move in September, October, and December, bringing total cuts to 75 basis points in 2025 and pushing the Fed funds target range down to 3.50–3.75%.

For additional context, we had already seen three rate cuts the year prior, in 2024—though that easing cycle began more aggressively. The Fed delivered a 50 bps cut in September 2024, followed by 25 bps cuts in November and December, totaling 100 basis points for the year.

Taken together, the Fed has now reduced rates by 175 basis points across 2024 and 2025, bringing the upper end of the federal funds rate down from 5.5% to 3.75%, where it stands today.

On this call, I was spot on—bullseye. The Fed did, in fact, cut rates more than twice.

Naturally, the latter part of the macro discussion turned to equities. So how did the stock market respond? Even though many had only priced in two rate cuts earlier in the year, the S&P 500 is up 17% YTD at the time of writing, sitting squarely at all-time highs.

This outcome lines up closely with my earlier prediction:

“As for the stock market, I expect solid performance in 2025, though not as strong as the last two years. The S&P 500 gained 25% in both 2023 and 2024, and it’s unlikely we’ll see another 25% jump. A more tempered increase of 15–20% feels realistic. The current market excitement feels a bit overextended, and it’s hard to see this rally sustaining the same momentum.”

However, the year didn’t start smoothly. In Q1, the S&P 500 fell roughly 19%, prompting some analysts to declare the onset of a bear market. That call proved premature. Instead, markets rebounded sharply, with prices rallying 44% from the trough and leaving the index up about 17% overall for the year.

The early-year drawdown was largely driven by fears of AI overinvestment—most notably around NVIDIA. This period became known as the “DeepSeek era.” A new Chinese entrant demonstrated AI models that were competitive with, and in some cases superior to, OpenAI’s GPT, yet built at a fraction of the cost. The implication rattled markets: if cutting-edge AI could be developed with far less compute, perhaps massive CAPEX spending wasn’t necessary after all. That narrative, in turn, raised concerns about future demand for NVIDIA’s chips, cascading into fears around revenues, valuations, and the broader AI trade.

As those concerns took hold, investors began to seriously question whether they were simply overpaying for equities. The second leg of the sell-off followed shortly after, triggered by Trump’s announcement of new tariffs on what was branded “Liberation Day.”

The policy introduced a baseline 10% tariff on all U.S. imports, with reciprocal tariffs exceeding 10% for several countries. China was hit the hardest, facing tariffs as high as 145%.

Markets reacted violently. Stocks suffered their worst two-day loss on record, with single-session declines ranging from 4% to 6%. In just 48 hours, roughly $6.6 trillion in market value was wiped out. Days later, however, Trump partially walked back the policy, announcing a 90-day pause on the tariffs.

Ironically, that moment marked the market bottom. From there, prices moved almost in a straight line higher over the next three months.

NVIDIA has since surged 117% from the April lows and is up 41% year-to-date, cementing its position as the most valuable company in the world with a market capitalization of $4.6 trillion.

Taking the macro section as a whole—particularly the calls around rate cuts and overall equity market performance—I’d score this one a 5. The thesis played out almost exactly as expected.

Score: 5

02/ Bitcoin

This is usually the most closely read section of an investment memo, since everyone wants to know what’s likely to happen to Bitcoin. It remains the centerpiece of crypto, the asset with the deepest relevance, the strongest institutional appeal, and the clearest signal for the rest of the market. Bitcoin leads, and the rest of the industry follows; its trajectory often becomes the industry’s trajectory.

For Bitcoin, however, one factor still matters more than anything else: price. Bitcoin’s price is its primary form of marketing. While there have been growing attempts to make Bitcoin more expressive — enabling things like NFTs, staking, smart contracts, and payments — none of these have meaningfully altered its core value proposition yet. They remain peripheral features, more additive than transformative. In other words, price continues to dominate Bitcoin’s narrative and adoption.

At the time of writing, Bitcoin is trading around $90k, down roughly 4% year-to-date. That headline, however, hides important context. Earlier in the year, Bitcoin was up as much as 35%, peaking around $126k in October, which makes the current drawdown more a function of volatility than a lack of interest.

Against that backdrop, I was directionally right. Price reached, and briefly moved beyond, my bearish case, but it failed to achieve either my base or bullish scenarios.

“My bullish case for 2025 is $170K, the base case is $150K, and the bearish case is $120K. If I had to pick a target to sell everything, it would be $150K — the level I’m most confident in, representing a 45% increase from the current $103K.”

What almost no one anticipated, myself included, was that Bitcoin would end up down on the year. That outcome caught many investors off guard, which underscores just how difficult forecasting truly is, especially when it comes to price.

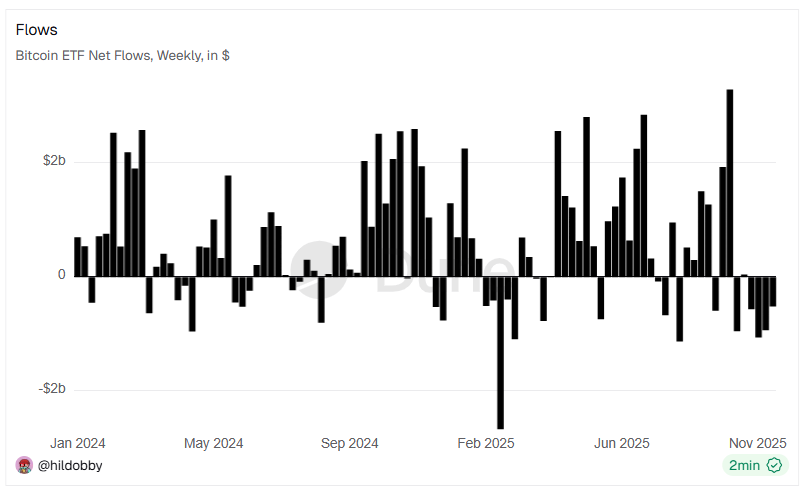

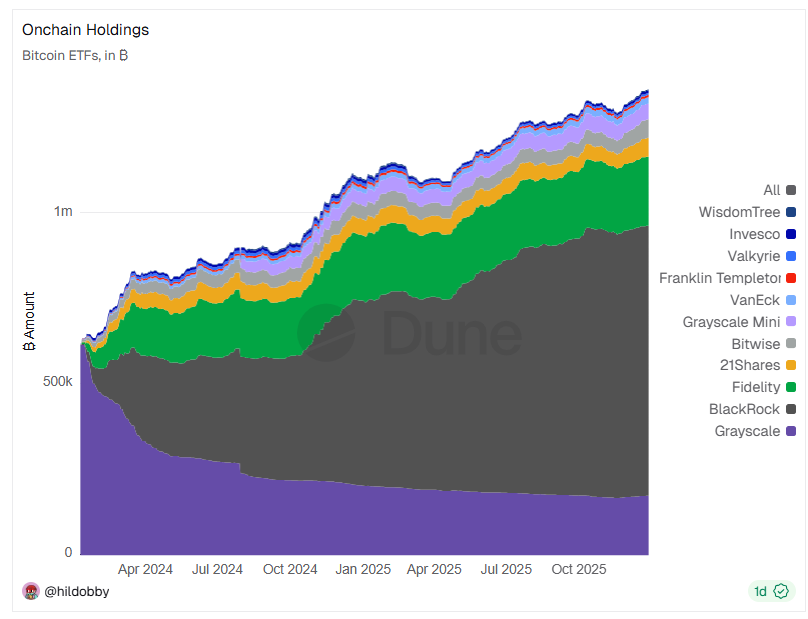

Turning to Bitcoin ETFs adds more nuance to the picture. In 2025, they recorded roughly $22B in net inflows. Hildobby’s dashboard doesn’t yet reflect data from the past month; however, using November figures as a reference, it’s reasonable to assume aggregate net inflows averaged closer to $20B for the year.

Those net flows, however, are heavily influenced by Bitcoin’s price, which is down year-to-date. Looking past dollar values and focusing instead on actual BTC movements tells a clearer story. In 2025, ETFs recorded 262,131 BTC in net inflows. Total holdings rose from 1,101,948 BTC at the start of the year to 1,364,079 BTC at the time of writing, currently valued at roughly $123B at a Bitcoin price of $90,000.

In that context, 2025 was relatively muted compared to 2024, which saw $38B in net inflows and 509,300 BTC added. By comparison, this year fell short of my 2025 expectations by roughly 50%.

“While inflows will likely grow, I don’t see that number doubling in 2025. Instead, I estimate around $45–50 billion in net inflows. The previous year’s rush was driven by TradFi FOMO and a booming stock market, but with markets likely taking a breather this year, Bitcoin ETF flows should follow suit.”

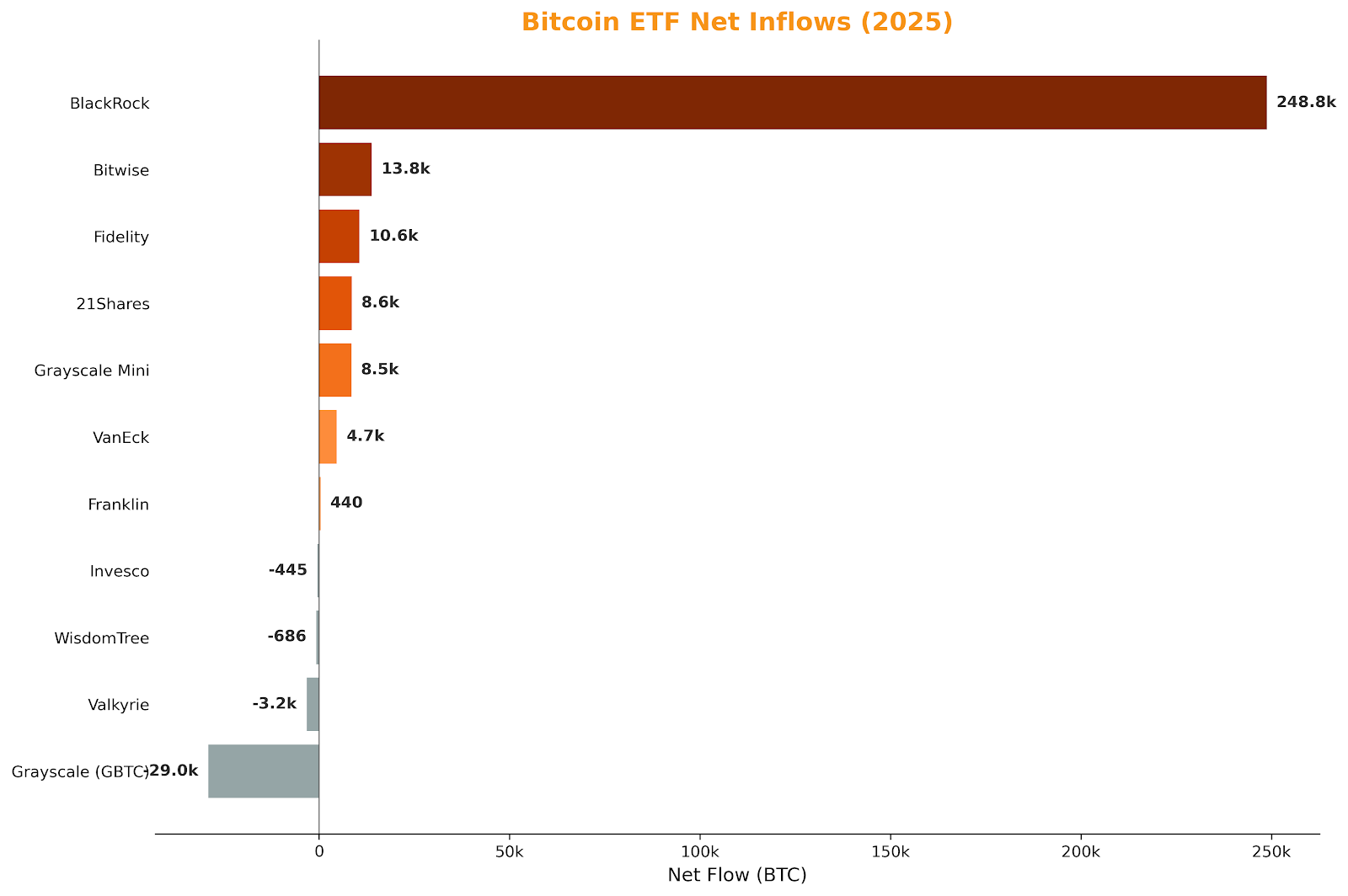

Flow concentration also stood out. BlackRock accounted for over 95% of net ETF inflows, adding 248.8K BTC. Bitwise and Fidelity followed at 13.8K BTC and 10.6K BTC, respectively, while Grayscale recorded the largest outflows, shedding 29K BTC.

Beyond flows, we also saw an expansion in ETF launches this year, largely in line with what I expected.

“This year, we could also see innovative ETF products, such as mixed-asset ETFs incorporating various cryptocurrencies. Regardless of how they’re packaged, 2025 will be the year of more ETF launches… An XRP or Solana ETF — or another unexpected contender — will likely be approved, but the market response may underwhelm, revealing a lack of appetite for diversification beyond BTC and ETH.”

That prediction broadly played out. Solana (SOL) ETFs launched from issuers including Bitwise, VanEck, Grayscale, Fidelity, and 21Shares. Ripple (XRP) ETFs followed from Grayscale and Canary Capital. We also saw ETFs tied to Litecoin (LTC) and Hedera (HBAR) reach the market.

In addition, a wave of multi-asset crypto ETFs launched, holding combinations of BTC, ETH, SOL, XRP, and others. These came from issuers such as 21Shares, Hashdex, Franklin Templeton, Grayscale, and Bitwise.

Netting it all out, the results were mixed. I was directionally right on Bitcoin’s price, which hit my bear case but missed my base and bull scenarios. I was wrong on ETF inflows, where my estimates proved too optimistic. And I was spot-on when it came to the pace and breadth of ETF launches.

Overall, I’d give this section a score of 3.

Score: 3

03/ Ethereum

Ethereum got its first real wave of DATs this year — and, more importantly, it got its Michael Saylor in Tom Lee.

DATs are publicly traded companies that pivot their entire business model toward accumulating crypto, typically Bitcoin or Ethereum. They raise capital by issuing new shares or bonds, often convertible debt, and deploy those proceeds directly into crypto purchases.

What makes this structure powerful is the feedback loop it creates. If a company’s stock price rises faster than the underlying crypto, it begins trading at a premium to its NAV (net asset value). As long as that premium exists, the company can issue additional equity, buy more crypto, and do so without diluting existing shareholders. In other words, “crypto per share” becomes the key KPI — and ideally, it compounds over time.

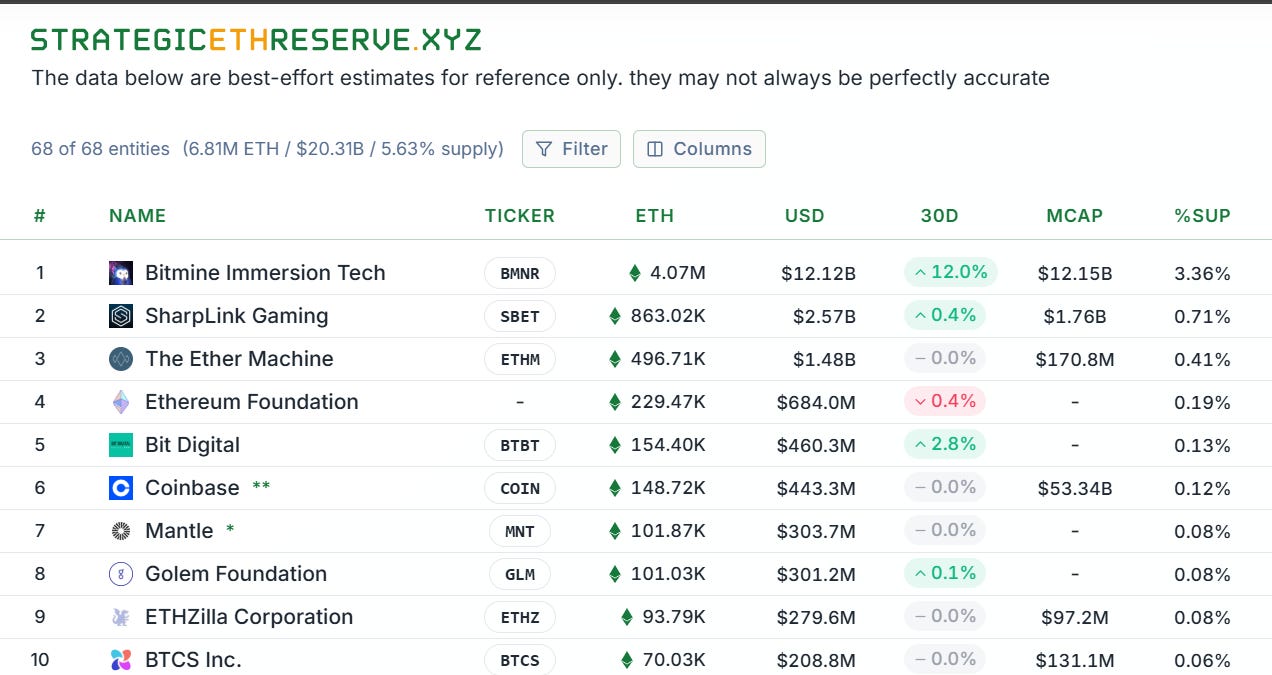

That dynamic is no longer theoretical for Ethereum. Collectively, Ethereum-focused DATs now own 6.81 million ETH, or 5.63% of total supply, valued at roughly $20.3B. Bitmine stands out as the clear juggernaut, holding about $12B worth of ETH, roughly 4.07 million coins.

Tom Lee has been explicit about his ambition to acquire 5% of Ethereum’s total supply. Today, he’s already about 67% of the way there, controlling roughly 3.36%. At first, many dismissed this target as a joke. On second thought, the prevailing assumption became that ETH would need to trade north of $10k for such a scenario to materialize.

Yet here we are: Tom Lee is already more than halfway to his stated goal, and ETH is still under $3k.

In addition, there’s meaningful participation from well-known players like Joe Lubin of SharpLink Gaming and The Ether Machine, each of which holds over $1B in ETH. Together, they represent the top tier of Ethereum-focused DATs, reinforcing how concentrated — and serious — this trend has become.

While I didn’t explicitly include DATs in my original predictions, I need to introduce them here as context for something we’ll revisit later. Before getting there, however, it’s worth grounding the discussion in how ETH actually performed in 2025.

This price action aligns closely with my ETH outlook going into the year.

“Assuming the gap between ETH and BTC narrows slightly in 2025, ETH’s upside could align more closely with BTC’s best-case scenario. Should BTC reach my $170k bullish target (+65%), ETH could gain between 45% and 50%, reaching $4,900 at best. However, my base case for ETH remains $4,300, with a flat-year scenario leaving ETH around $3,300. While Ethereum’s long-term potential remains compelling, 2025 is unlikely to see it reclaim the dominance it’s lost to Bitcoin this cycle.”

What stands out is that ETH didn’t just meet my base case — it briefly reached my best-case scenario without BTC ever touching $170k. For a short window, it genuinely looked like ETH was outperforming Bitcoin.

That relative strength shows up clearly in the ETH/BTC ratio. While it’s down 5.17% on the year, it surged as much as 143% between April and August. For context, that four-month stretch marks ETH’s strongest relative performance versus BTC since early 2021, when ETH outperformed Bitcoin by more than 200% in the first four months of the year.

So what drove this outsized ETH outperformance relative to BTC?

DATs.

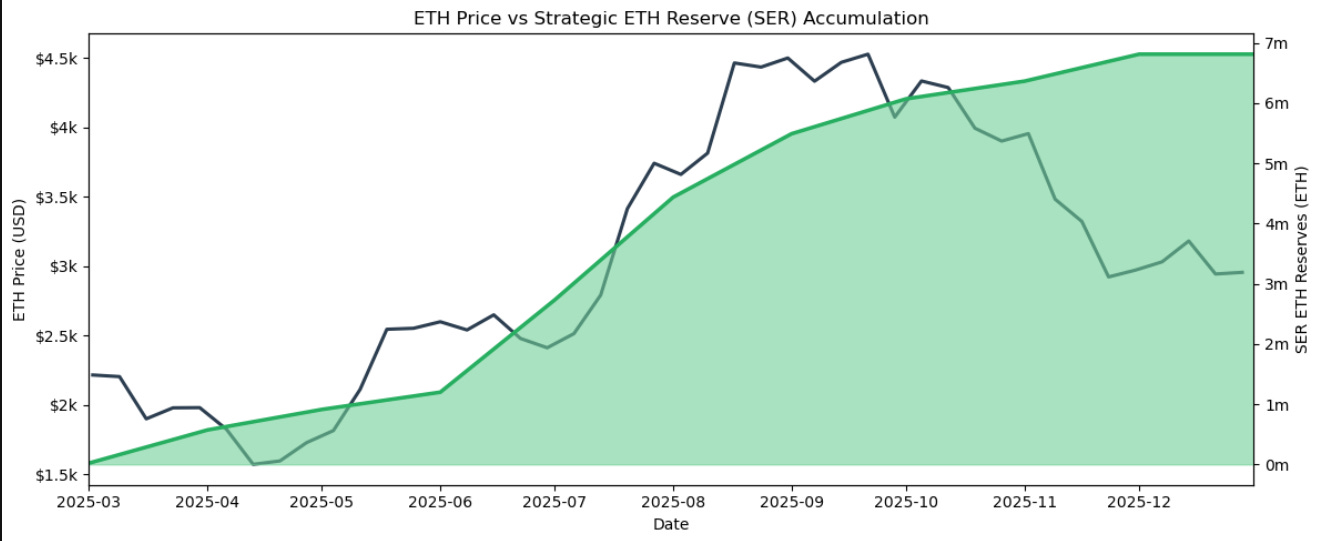

When you overlay ETH’s price action with the growth in Strategic ETH Reserves (SER), the relationship becomes hard to ignore. Between April and August, roughly 4.9 million ETH — about $21.7B worth — was added to the balance sheets of Ethereum-focused DATs. That accumulation window lines up almost perfectly with ETH’s rally.

In other words, this wasn’t random outperformance. It was structurally driven by demand.

Now, I’m not saying DATs were solely responsible for the move. However, it’s difficult to dismiss the impact of a $20B+ bid hitting an asset over just a few months. That kind of demand doesn’t emerge in a vacuum. In fact, there’s a strong case that without the DAT-driven buying pressure, ETH’s price today would be materially lower than where it currently sits.

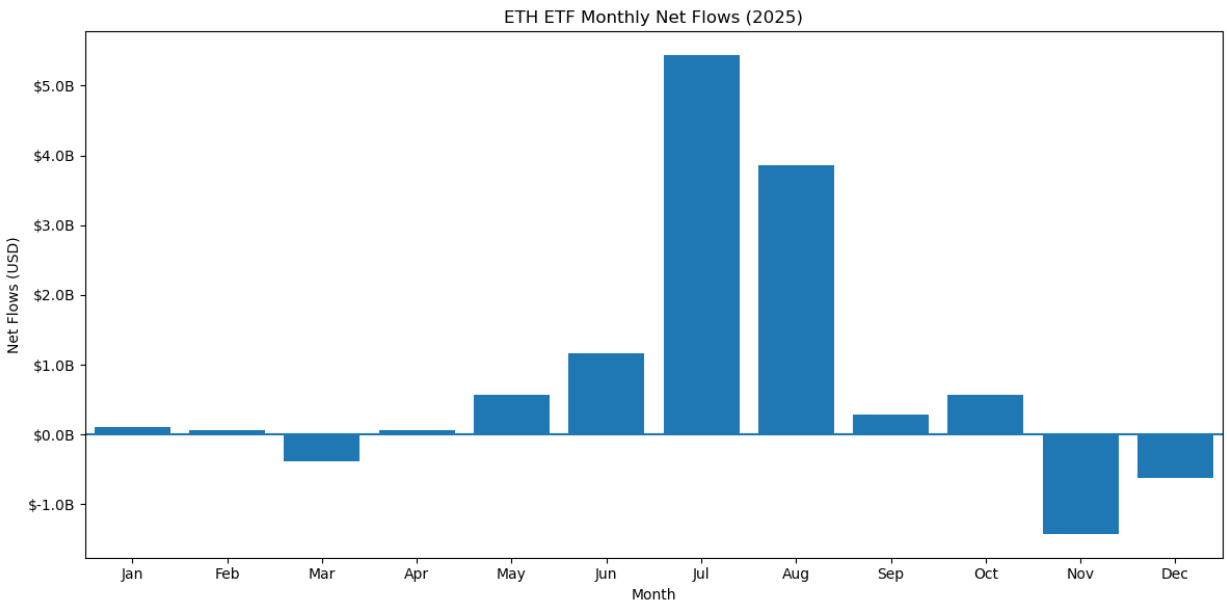

Turning to Ethereum ETFs, they recorded $9.68B in net inflows in 2025, well below my earlier projection that demand would double.

“ETH ETFs have already attracted $12 billion in net inflows, despite being less than a year old. I anticipate that figure doubling in 2025, pushing total assets under management (AUM) to ~$40 billion by year-end.”

That forecast missed the mark. Ethereum ETF AUM ended the year at $18.51B. While that still represents growth, it came nowhere near the pace many — myself included — expected.

As a result, for the second year in a row, Ethereum ultimately proved to be the inferior asset when compared to Bitcoin.

On the Layer 2 front, however, I got this one right. As an investment thesis, L2s continued to underperform — exactly as expected.

“On the other hand, Layer 2s (L2s) continue to underperform the broader market. The sector’s outlook is bleak. My advice? Sell into every pump. I once strongly believed in the L2 investment thesis, but that view has since changed. Modular blockchains haven’t proven to be as revolutionary as once promised. With more than 150 Ethereum L2s now in existence, the space is overcrowded and undifferentiated. Even among the largest projects by market cap, genuine innovation is hard to find. Many are effectively alt-L1s or simple EVM clones.”

The largest L2s by market cap — including Mantle, Arbitrum, Optimism, and Polygon — are down roughly 65% on average over the past year.

So how does this section score?

I was directionally right on ETH price, materially overestimated ETF inflows by roughly 60%, and correctly called the continued weakness of the L2 investment thesis. Taken together, a score of 4 feels fair.

Score: 4

04 / Supercycles

I was never fully on board with the wave of financial nihilism that took hold about a year and a half ago — the idea that investing in crypto is pointless because everything eventually goes to zero anyway, so we might as well gamble on memecoins until the end. That mindset, in turn, gave rise to the entire memecoin supercycle narrative.

In hindsight, that thesis failed almost immediately. The moment it became widely discussed was effectively the moment the trade began to die. Murad emerged as the de facto Satoshi of this narrative, and his picks became a useful bellwether for the broader sector. They didn’t age well. His top five memecoin selections are down roughly 80% on average over the past year, which speaks volumes about where the memecoin market ultimately ended up.

In my 2025 predictions, I wrote:

“There’s no such thing as a memecoin supercycle. While we may see occasional rotations into memes, that doesn’t make it a true supercycle. Each rotation will favor a different meme, so holding onto any of Murad’s picks might not be the best strategy. With only a year left in this cycle, it’s unlikely that any new memecoin will surpass Doge, Shib, or Pepe. I used to think otherwise, but my outlook for the year has changed.”

That view held up. There were rotations, but no supercycle, just brief bursts of speculation that burned out as quickly as they appeared.

As a result, Doge, Shib, and Pepe remain the three largest memecoins. The idea that one of Murad’s picks, or any newer meme, would eventually flip one of the top three never materialized.

The second part of this section, however, is where I was flat-out wrong.

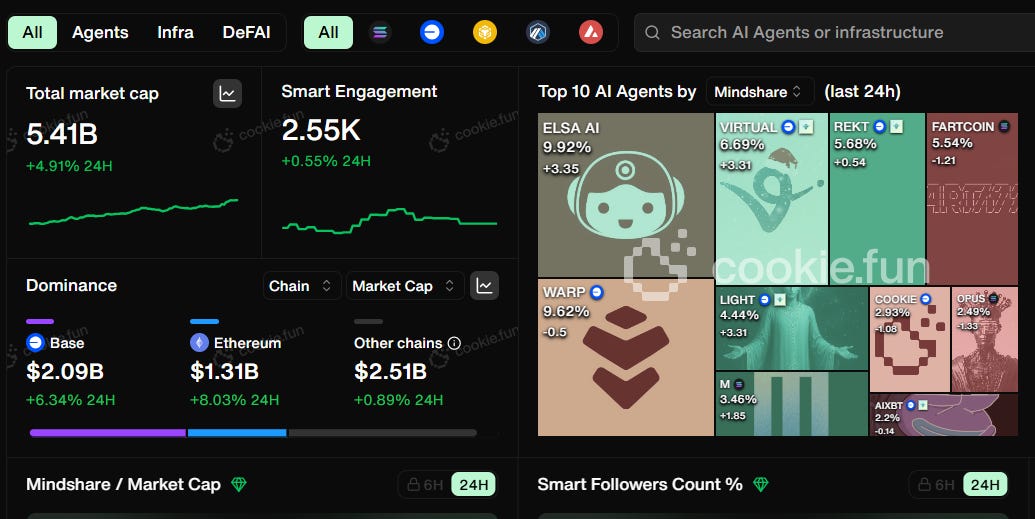

I got swept up in the AI-agent hype cycle last year and convinced myself there might be something structurally meaningful there. I tried to stay cautious, but even that caution proved too optimistic. The sector ultimately peaked around $30B — far short of my $120B projection, which at the time felt conservative relative to the $200B–$250B targets others were calling for.

Here’s what I wrote then:

“On the other hand, AI agents will dominate the meta this year, potentially reaching memecoin-like valuations of over $120B by the end of the year. Not because they live up to the hype, though. In reality, most of these are just chatbot wrappers — useful, yes, but not groundbreaking. It’s crucial to adjust expectations and recognize what we’re dealing with.

Some are calling for AI agents to hit $250B (or even $500B in extreme cases), likening it to DeFi Summer in 2020. I think they’re getting ahead of themselves. People will soon realize these tools aren’t genuinely autonomous or agentic. They will always require human oversight — though that’s not necessarily a bad thing. The challenge lies in balancing expectations with reality.

By the end of the year, the winners in crypto might look very different from what they are today. This pattern is classic in the space. Remember this time last year? AI infrastructure projects were the golden child of the crypto × AI narrative. Now, the spotlight is on AI agents. By the time I revisit this review, it could be something else entirely. Regardless of who the individual winners are, the ecosystem will continue to evolve and grow.”

In hindsight, even that framing gave the sector too much credit. The hype peaked early, valuations stalled, and the supposed “agentic” breakthrough never arrived.

Looking back now, there’s no meaningful AI × crypto meta to speak of. It effectively died in January.

To be fair, I adjusted my bias on AI agents relatively early and walked back most of my initial assumptions in subsequent research, laying out a clear bear case for the sector — with the lone exception of DeFAI. Even that exception, however, failed to develop any real staying power.

I ultimately threw in the towel on the entire theme in Muse #18: Thoughts on a Bear Market, Cycle Peak, and Reflections.

The total market value of AI agents, including DeFAI, now sits at $5.41B, down more than 80% from the peak.

This was the first time I had to formally walk back a prediction. I had a thesis, but within a month the data shifted enough to invalidate it — so I adjusted accordingly. In hindsight, exiting AI-agent or broader AI × crypto positions back in February was a gift. The entire space has been relentlessly sold off since.

At this point, I think the sector is genuinely over, in much the same way the gaming narrative was finally laid to rest in 2024.

I got the memecoin call right, but missed badly on AI agents. Taken together, that balances out to a 3 for this section.

Score: 3

05 / Wildcards

The only investment that even came close to working this year was Hyperliquid (HYPE). At one point, it was up roughly +140%, yet it ultimately closed the year essentially flat, finishing around +5%. Sui, meanwhile, peaked in January — right around when I published my initial predictions — and then went on to fall roughly 66%. Berachain did eventually launch, but it turned out to be a complete disappointment.

That outcome stands in stark contrast to my earlier expectations:

“The alt-L1 trade will resurface yet again, as if it never left. This time, however, it likely won’t center on Solana. Instead, projects like Sui and Hyperliquid seem poised to take the spotlight as the most promising contenders. We might finally see Berachain launch and join the race as well. Other alt-VM chains, like Aptos and Sei, remain in the mix, but they feel more like beta plays — or perhaps theta plays — relative to Ethereum.”

In reality, the alt-L1 trade never materialized. There was a brief moment mid-year when it looked like Hyperliquid might lead the charge, but that momentum faded quickly. By year-end, everything was down, including Ethereum and Bitcoin, and the broader alt-L1 thesis failed to play out.

This was a typo, not a miss.

At the time of writing, stablecoin supply was already around $200B, and the prevailing consensus was that it would double toward $400B. I intended to reference that higher figure, but mistakenly wrote $200B instead.

My actual forecast was for stablecoin supply to exceed $250B, with a peak closer to $280B — not the $150B–$180B range stated below:

“On the stablecoin front, supply will increase but likely won’t hit the $200B mark that many are forecasting. I expect a more muted year for markets overall, with the Fed cutting rates and reducing yields, which will dampen demand for stablecoins. That said, stablecoin supply should exceed $150B by year-end, potentially peaking around $180B.”

In reality, stablecoin supply surpassed $300B in December. That outcome validated the higher-level direction of the call, even if the published numbers were incorrect.

Turning to individual stablecoins, USDe did gain traction — but it failed to sustain it.

Supply expanded from $5.8B at the start of the year to a peak of $15B in October, only to unwind back to $6.2B by year-end. That’s a net increase of just 6.4%, which is effectively flat by crypto standards.

USD0 performed even worse. Its market cap collapsed by roughly 70%, falling from $1.8B to $547M at the time of writing.

That outcome diverged from my earlier view:

“USDe will continue gaining traction, steadily eating into the market share of giants like USDT and USDC. Additionally, we’ll likely see the rise of alternatives like USD0. For what it’s worth, I believe the combined market dominance of USDT and USDC has already peaked — especially USDT’s. The era of unquestioned dominance for these two stablecoins may be behind us.”

In hindsight, that call was only partially right. USDT’s dominance has peaked; however, combined USDT + USDC dominance has not. USDe — the primary challenger expected to take a meaningful share, ultimately ceded ground.

Today, USDT and USDC still account for roughly 88% of the total stablecoin market share. USDT’s share declined from ~70% at the start of the year to ~64% now, while USDC gained share, rising from ~22% to ~25%.

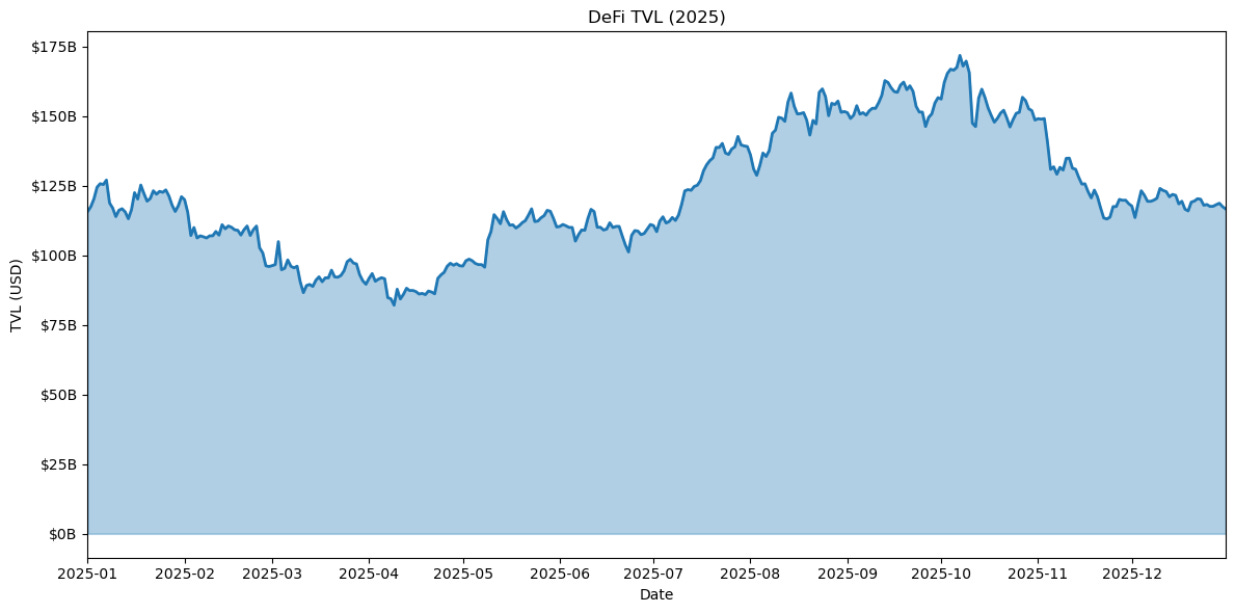

DeFi TVL did hit my target almost exactly. Total value locked peaked at $172B, broadly in line with expectations. However, performance over the year was effectively flat — DeFi started the year at $115B and closed at $116B. Notably, this marks the first time in DeFi’s relatively short history that TVL neither meaningfully grew nor declined over a full year.

“DeFi’s total value locked (TVL) is likely to hit $150B, with a potential peak around $170B. While we’ll continue to see hype cycles driven by new or evolving DeFi products, the sector as a whole is set to grow steadily.”

NFTs, on the other hand, are effectively dead — and this time, there wasn’t even the usual short-lived revival we tend to see every 6–9 months. There isn’t much more to add.

“As for NFTs, they won’t return to their 2021 glory days. After this year, the sector will likely settle into a cycle of underperformance, finally earning the ‘dead’ label — and this time, it might stick. While NFTs will still perform well in some pockets, the overall growth will remain unimpressive.”

Overall, this section was a mixed bag. Some calls were directionally right earlier in the year — such as USDe traction and the initial signs of an L1 rotation — but failed to hold by year-end. The L1 trade, if we’re being strict, never truly materialized. Stablecoin growth, however, was on point, and the TVL and NFT calls were also accurate.

Taken together, a 4 feels fair.

Score: 4

06 / Value Traps

The only clear-cut value trap this year was Layer 2s — exactly as I warned in the Ethereum section. Beyond that, however, the bigger trap was more subtle: our expectations for how 2025 would actually play out.

I approached the year with cautious optimism, already assuming it would be slow. Even then, reality undershot those expectations. 2025 wasn’t just slow — it was underwhelming, and by year-end, that reality became hard to ignore.

Here’s what I wrote at the time:

“The key value trap this year is overestimating. Lower expectations on any prediction by about 30% as a safeguard. Another notable trap is the Layer 2 investment thesis. While L2s remain essential for scaling, they may not deliver the financial returns many are hoping for.

I also expect the market to peak later in the year — likely in Q4, with August as my base case. With that in mind, Godspeed!”

The market did peak in Q4, though slightly later than expected — in October. So far, that remains the high, and if 2026 does turn into a bear market, it will likely stand as the cycle peak. But that’s a question for next year’s predictions.

Overall, this section aged well. It was right on L2s and, more importantly, right on expectations — both in terms of market structure and overall pacing.

Score: 5

Conclusion

This marks the second annual review of my predictions. If you’re curious, you can also read the 2024 predictions review. Last year, I scored 76% — a solid result by any academic standard, comfortably an A, with most cutoffs starting at 75%.

So how did this year stack up?

I broke the 2025 outlook into six major sections:

Macro: 5

Bitcoin: 3

Ethereum: 4

Supercycles: 3

Wild Cards: 4

Value Traps: 5

That adds up to 24 out of 30, or an 80% accuracy rate, exceeding last year’s score.

A fair result, if you ask me, especially given how unusual and difficult 2025 was for most market forecasts. Consistency matters, and repeating an A in a year where many narratives completely broke down isn’t something I’ll complain about.

My 2026 predictions will be out soon.

Until then — peace.